Creation of Medicare and Medicaid—Significant Healthcare Event

Abstract

Medicare and Medicaid came into legislation on July 30, 1965 with a signature from President Lyndon B. Johnson and have demonstrated changes on health-care in the short-term sense, long-term sense, and the historical evolution of health care as a whole. The programs have contributed to the formation of the Affordable Care Act, and came with their own set of anticipated outcomes and unexpected problems. Medicare and Medicaid has taken over the discussions among healthcare professionals, political leaders, and community members; therefore, it is crucial for members involved in these conversations to understand the range of sub-topics from both perspectives to better understand the two programs that cover some of the most under-served, at risk members of our communities.

How does this significant event/concept change in healthcare in the short-term?

A main barrier that senior citizens face when seeking medical care is the ability to follow-through with post-care after they get home. A substantial amount of senior citizens are able to live independently while maintaining their sense of healthy aging; however, there are also a significant amount of senior citizens who still need assistance living independently and more so, would require assistance after a medical procedure is completed. Short-term care is offered to senior citizens who are covered by Medicare after they have received their medical treatment. Unfortunately, some medical treatments require a longer recovery time, and if the patient falls under the category of senior citizens whom require assistance to complete daily tasks, then the individual can often find themselves paying for long-term care services and assistance “out of pocket by, private insurance, or by the Medicaid program for those with low incomes and assets” (Davis & Collins, 2005-2006). Initially, a main barrier for senior citizens to receive medical treatment was the lack of support or assistance with daily tasks during recovery time; however, a second barrier is added once the individual has to acknowledge that there are extensive costs that come with long-term treatment that may not be covered by Medicare. According to the National Institute on Aging, the Medicare/Medicaid program “does not cover ongoing personal care at home” (NIA 2017). A third barrier for senior citizens in need of medical treatment is added once the patient realizes that their long-term recovery process may not be possible to complete while in the comfort of their own home and may require an extensive stay at the hospital. The Fact Sheet for Short-Term, Limited-Duration Insurance Proposed Rule states that “this type of coverage is exempt from the definition of individual health insurance coverage under the Affordable Care Act (ACA) and is therefore not subject to the ACA provisions that apply to individual health insurance plans (“Fact Sheet: Short-Term, Limited-Duration Insurance Proposed Rule”, 2018). While Medicare can assist patients with relief from payment on a plethora of services, and even has sub-programs that assist patients living with specific chronic illnesses, Medicare and its sub-programs only cover specific categories of care that a patient may or may not be experiencing. PACE—a sub-program from Medicare—assists patients who are struggling with life-long illnesses such as Alzheimer’s or Dementia, but lacks any substantial assistance for senior citizens who are attempting to recover from a one-time medical procedure or preventive care.

What were the long – term effects?

Although both Medicare and Medicaid serve long-term care for underserved community members, the programs are hindered by existing gaps in services and overlap in patient care. Patients experiencing chronic illnesses and/or a plethora of different disabilities are eligible for long-term care benefits for ninety days or more. The majority of long-term care is provided by members of the patient’s family and friends whom are already living with their own sets of families. Formal long-term care—which is often paid for by government sources—is described by H. Stephen Kaye, Charlene Harrington, and Mitchell P. LaPlante as: 1. “Home and community-based services” where the patient receives additional assistance in the comfort of their own homes, and 2. “Institutional care” where the patient is cared for by a team in an alternative setting, such as a nursing home or a care facility. (Kaye, Harrington and LaPlante, 2010).

Together, Medicare and Medicaid pay the highest percentage of the total cost for long-term care. According to the National Health Expenditure Accounts Team consisting of Micah Hartman, Anne Martin, Aaron Catlin, and P. McDonnell, in 2007, the total costs for nursing home and home health care in the United States was estimated at $190.4 billion. Of that total estimated cost, “Medicare paid for 25 percent, Medicaid and other public funds paid for 42 percent, out-of-pocket funds paid for 22 percent, and private insurance and other sources paid for 11 percent (excluding hospital-based nursing home spending)” (Hartman, Martin, McDonnell and Catlin, 2009).

Although both Medicare and Medicaid paid for the highest percentage of long-term care, the programs derived from different places of origin and were created to cover different groups of community members. Medicare operates at the federal level only, while Medicaid operates at both federal and state levels. H. Stephen Kaye, Charlene Harrington, and Mitchell P. LaPlante explain in their article “Long Term Care: Who Gets It, Who Provides It, Who Pays, and How Much?” how “the resulting variation among states’ budgets and coverage decisions adds to the overall complexity of public programs’ services and spending within and across states” (Ng, Harrington and Kitchener, 2010). Although post-acute care through Medicare and long-term care services through Medicaid can appear to be kindred in the goals they set for the patients they serve and the communities they represent, the programs execute practices and workflow that are poorly uncoordinated and counterproductive, while also withholding incentives that compete amongst one another. Terence Ng, Charlene Harrington, and Martin Kitchener focus on several of the main problems that Medicare and Medicaid are experiencing regarding long-term care. In their article “Medicare and Medicaid in Long Term Care”, the authors analyze the situation and circumstances of long-term care under Medicare and Medicaid and argue that “Medicare focuses on limiting hospital and post-acute use and costs, resulting in shifts in care to the Medicaid long-term care program. That program has little incentive to reduce Medicare hospital and emergency room use.” (Ng, Harrison and Kitchener, 2010). If these issues are going to be resolved among the healthcare system, then changes in policy are critically necessary in order to align the incentives, goals, and measurable outcomes for the two programs that will continue to serve our most vulnerable, at-risk, and underserved populations.

How Medicare and Medicaid impacted the historical evolution of healthcare

Before President Lyndon B. Johnson signed Medicare and Medicaid into legislation in 1965, many middle-class employed Americans were utilizing private pay health care insurance; unfortunately, not all citizens could afford to pay for private health care insurance, so many senior citizens, unemployed citizens, and citizens living in poverty were forced to go without medical treatment, necessary prescriptions, or had to seek help from public programs that were already short in supply. At this point in time, about half of senior citizens had access to health care services, and most of them were living at various levels of poverty. Thankfully, groups of health care workers—both providers and nurses alike—saw that there was a desperate need in their communities and offered to volunteer their time and expertise to underserved, at-risk patients at no charge. When Congress passed the Social Security Act, the Medicare and Medicaid programs were not far behind. Leiyu Shi and Douglas A. Singh describe the progression thereafter by stating that “the government then was responsible for paying for some of the health care. In the end, a three-layered program emerged. The first two layers constituted Part A & Part B of Medicare, or Title XVIII of the Social Security Amendment of 1965, and was to provide publicly financed health insurance to the elderly” (Shi & Singh, 2014, pg. 103-104). The Medicare and Medicaid programs catered to Americans 65 and older by providing them with accessible hospital care, extended care after the hospital stay was complete, along with at-home care, as well. Although the benefits that Medicare and Medicaid were providing to the senior citizens of America were substantial, there was still a need to be met among other populations. Medicare and Medicaid then offered the states the option to provide accessible health care to children living in low-income households, the caretaker relatives, citizens experiencing blindness, and individuals with disabilities through federal funding.

Medicare and Medicaid’s contributions to the formation of the Affordable Care Act

While costs of health care have remained a barrier to underserved populations for generations, there have consistently been attempts to alleviate that stress, destroy the barrier, and attempt to provide affordable health care access to all citizens—regardless of their demographics, location, or income. In 2010, the Patient Protection and Affordable Care Act (ACA) attempted to help destroy the access barrier by providing a second option for those who did not qualify for Medicare; however, when voting season arrived in 2013, “only 25 states confirmed participation in Medicaid expansion, and 26 states declined state-run health insurance exchange” (US Department of Health & Human Services). Although the name “Affordable Care Act” seems rather straightforward and to the point of the goals they are trying to achieve, the program has milestones to reach before it can live up to its name.

“In the fourth quarter of 2016, a short-term, limited-duration policy cost approximately $124 a month compared to $393 for an unsubsidized ACA-compliant plan. Based on enrollment trends prior to the October 2016 final rule, the Departments project that approximately 100,000 to 200,000 additional individuals would shift from an ACA-compliant individual market plan to short-term, limited-duration insurance in 2019. Only about 10 percent of these individuals would have been subsidy-eligible if they maintained their Exchange coverage” (“Fact Sheet: Short-Term, Limited-Duration Insurance Proposed Rule”, 2018).

These staggering statistics show that while the “Affordable Care Act” program is not living up to its name quite yet, the majority of citizens are going to stick with their short-term, limited-duration insurance plans due to reduction of costs.

Medicare and Medicaid’s unanticipated outcomes

Like all new programs introduced to the public, the Medicare and Medicaid programs accumulated a set of unanticipated outcomes. While technical glitches can usually be fixed in a timely manner, the Department of Health and Human Services have been working diligently to ensure that the unanticipated outcomes and technical glitches get resolved as quickly as possible so that Medicare and Medicaid can be successful programs for citizens living in all 50 states. New programs will also inevitably also have its companies with doubts and concerns; in 2013, the New York Times featured an article that stated, “Whether the exchange program will have the capacity to ensure access and quality of care comparable to those of current Medicare is a matter of great uncertainty: if the number of younger and healthier enrollees significantly falls behind the target number, the financial base of the exchange program will be jeopardized” (New York Times, 2013). The subject of affordable and accessible health care has been a hot topic for generators, and while our country is in the midst of a reform on health care, political leaders and policymakers alike are aiming to utilize surveys, certifications, payments, and penalties to control the suffocating costs that health care provides to the country’s citizens. Although the policymakers and political leaders are remaining active in the quest to achieve accessible and affordable health care, these tools undoubtedly also come with their own set of anticipated outcomes. Today’s health care system and is a complex puzzle and is described by Lewis A. Lipsitz as “nonlinear, dynamic, and unpredictable nature. Policy makers and physicians need to understand health care as a complex system and apply the principles of complexity science to achieve their goals” (Lipsitz,2012). In order to continue successfully researching different methods behind achieving affordable health care and the sociology behind the trends, policymakers, medical providers, and community members are going to have to understand and expect that with all great quests and experiments, there will always be unanticipated outcomes.

What new problems were created?

While attempting to alleviate the problem of unaffordable health care among Americans, especially the underserved population, the American people and its political leaders found an additional problem hovering above the country’s head. In order to address the U.S. debt crisis, a decision was ultimately determined to begin a federal budget reform which will have a direct impact on the Medicare program and all of the citizens that it covers. One example of a change in Medicare will be the age in which a senior citizen is able to receive benefits. The age to receive Medicare benefits would eventually rise from age 65 to age 67 in order to decrease the amount of people who may utilize the services in attempt to lower the U.S. debt. However, in 2013, both the White House and Senate Budget Plan rejected the proposal (Senate Budget Committee).

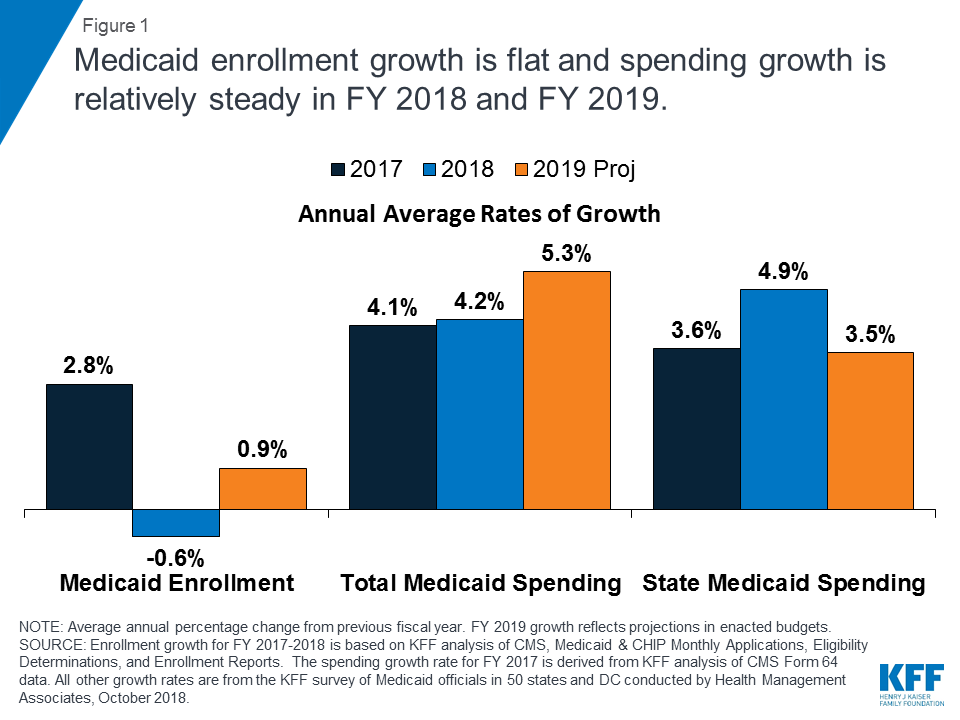

Today, America has maintained a stronger economy which has caused a slower enrollment rate for Medicaid and a steady growth on spending. Below is a chart that shows how Medicaid enrollment and spending growth are compared:

Conclusion

As the old saying goes, “history repeats itself”. Fortunately, American citizens have demonstrated the ability to analyze past situations and strategize to learn from our mistakes to avoid future downfalls. The reformation of healthcare systems is no different. If Americans are going to achieve accessible and affordable health care, political leaders, insurance companies, and medical providers alike need to focus not just on the elderly, but for the remaining at-risk, unserved patients, as well. Raising the age limit from 65 to 67 for Medicare eligibility has been established to accommodate senior citizens; however, Jinhyuan Yang, Chenxi Huang, and Preetha Phillips use their article to explain that:

“The marginal survivors who benefit from the generous coverage of Medicare at age 65 and 66 could suffer premature death if exposed to the risks associated with uninsured patients. Additionally, the seniors who can survive up to 67 with less generous insurance coverage at younger ages cold face faster deterioration of health because of less access to preventive care or prescription drug therapies, and consequently have greater health care needs and higher health care expenditures after age 67; such a course of events could offset the cost-saving purpose of the policy option to raise Medicare eligibility age” (Yang, Huang, & Phillips, 2014).

If health care not only became affordable and accessible to all citizens of America, but also adopted a “whole-person care” model, then the risks associated with coming into contact with “uninsured patients” would diminish and our country could potentially progress into the healthiest and lucrative generation of our time.

References

- Centers for Medicare and Medicaid Services (2015, July). Milestones 1937-2015. Retrieved from https://www.cms.gov/About-CMS/Agency-Information/History/Downloads/Medicare-and-Medicaid-Milestones-1937-2015.pdf (Links to an external site.)Links to an external site.

- Davis K, Collins SR. Medicare at forty, Health Care Finance Rev .2005–06: 27 (2:53–62. Medline, Google Scholar

- Fact Sheet: Short-Term, Limited-Duration Insurance Proposed Rule (2018). Retrieved from https://www.cms.gov/newsroom/fact-sheets/fact-sheet-short-term-limited-duration-insurance-proposed-rule

- Hartman M, Martin A, McDonnell P, Catlin A, National Health Expenditure Accounts Team. National health spending in 2007: slower drug spending contributes to the lowest rate of overall growth since 1998. Health Aff (Millwood). 2009: 28 (1): 246–61. Go to the article, Google Scholar

- Kaiser Commission on Medicaid and the Uninsured. [2012 cFeb]; Medicaid managed care: key data, trends, and issues. Retrieved from http://kff.org/medicaid/issue-brief/medicaid-and-managed-care-key-data-trends/

- Kaye HS, Harrington C, LaPlante MP. Long-term care in the United States: who gets it, who provides it, who pays, and how much does it cost? Health Aff (Millwood), 2010: 29 (1): 11–21. Go to the article, Google Scholar

- Lipsitz, L. A. (2012, July). Understanding Health Care as a Complex System the Foundation for Unintended Consequences. JAMA, 308(3), 243-244.

- New York Times. How healthcare.gov was supposed to work and how it didn’t. New York, NY: New York Times, 2013. Available at: http://www.nytimes.com/interactive /2013/10/13/us/how- the- federal- exchange- is- supposed- to- work- and- how- it- didn’t .html?

- Ng, T., Harrington, C., & Kitchener, M. (2010, January). Medicare And Medicaid In Long-Term Care. Health Affairs, 29(1), Retrieved from https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2009.0494

- Paying for Care. (2017, May 01). Retrieved April 30, 2019, from https://www.nia.nih.gov/health/paying-care

- Senate Budget Committee. Foundation for growth: restoring the promise of American opportunity: the fiscal year 2014 Senate budget resolution. Washington, DC: Senate Budget Committee, 2013. Available at: http://www.budget.senate.gov/democratic/ public /index.cfm/fiscal- year- 2013- budget.

- Shi, L., & Singh, D. A. (2014). Delivering Healthcare in America: A Systems Approach (6th ed.). (pp. 103-104). Sudbury, MA: Jones and Bartlett Publishers. ISBN 9781284074635

- U.S. Department of Health and Human Services. The Affordable Care Act. Washing-ton, DC: U.S. Department of Health and Human Services, 2013. Available at: HTTP:// www.hhs.gov/healthcare/rights/law/index.html

- Yang, Z., Huang, C., & Phillips, Victoria. (2014, August). Medicare Eligibility Age, Health Disparities, and Medicare Reform. Journal of Health Care for the Poor and Underserved; 25(3), 1379-83. Retrieved from https://search-proquest-com.csuglobal.idm.oclc.org/pqrl/docview/1557153055/8BC16A55C47543FAPQ/20?accountid=38569

Cite This Work

To export a reference to this article please select a referencing style below: